How To Budget Your Business Like A Film Producer

One thing I was never taught about business was how to budget.

I’d learned how to create a personal budget for myself and then later for my family, and we got it to a point where even though my wife and I are both freelancers with irregular income, we still figured out how to make it work, which includes things like buying a house, paying down $20k worth of debt in a year, and having some consistency in all of the chaos.

What I wish I knew was how to budget my business so that it could survive the ups and downs and ebbs and flows of irregular income, while still paying me a consistent salary every month, remaining profitable, and having enough in the bank to invest and grow.

In this chapter, that’s what you’ll learn how to do.

How To Budget Like A Film Producer

Feature films are interesting little mini-businesses that start when a chunk of money is given to a production company to make a movie, spent over a matter of months, and then (hopefully) turns a profit on the other end.

The producer is essentially the CEO of this little (or big) business, and the few movies I’ve worked on have had budgets that are similar enough to a small or one-person business like the ones we’re trying to build together through this book to be an appropriate analogy.

Part of my job as a film and tv producer is to create budgets for these films based on how much money is available to spend.

If, for example, I am told that we have $750,000 to spend on this movie, it’s then my job to give every one of those dollars a “job”.

This process of allocation is rule number one for budgeting your business.

You, however, don’t have film financiers, but you do have clients and customers.

My recommendation is to create a budget for the next three months, because who knows how things might change or grow in your business over a longer period of time like a year.

(Two years in a row my business doubled in revenue, which I was not anticipating in my annual budgeting session…)

First - Determine How Much You Have To Spend

So, take your last three months as a baseline, and assume that you’ll make the same amount for the next three months. If you make $7,000 per month, then your total amount to spend is $21,000.

On a film budget, one of the first line items—or jobs for the dollars I have in my budget—is a “contingency” line item.

In your budget, this would be “profit”.

Remember, we practice what we preach here, and we take our profit first.

So, out of your $21,000, you will take 2% or 5% or 10%, whatever amount you’ve decided on or are working toward. If you’ve never taken a profit before, set it at 1% or 2%.

Now, a quick aside to talk about tools.

You don’t need expensive software, and there aren’t any dedicated business budgeting tools that I’ve enjoyed using.

While I have Quickbooks for my accounting, I am not a fan of the budgeting feature, plus it costs extra.

One thing I currently do is I use YouNeedABudget.com and I tweak it a little for my business so that I can track accounts receivable, but we’re getting a bit into the weeds.

You can read about how to set it up on their blog, but if you don’t want to worry about learning something new, you can use a simple spreadsheet, which is what I’ll use for the diagrams and examples in this chapter.

Google Sheets even has an Annual Budget Tracker template that you can use which has a bunch of pre-built formulas and some nice design to it as well.

So, you start with what you have to budget, $21,000 in our example, and enter that on the first page of the template.

Budget Allocation - Give Every Dollar A Job

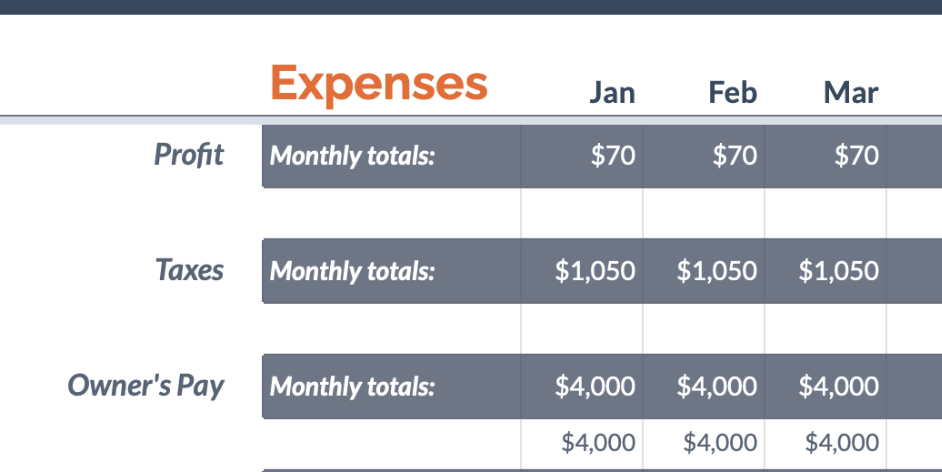

Next, you’ll want to rename the different budget categories and make the top three profit, taxes, and owner’s pay. For this example, I’ll just use 1% for profit.

I’ve got 15% of revenue set aside for taxes, and I want to pay myself $4,000 per month in salary. That comes to a total of $15,360, so we have $5,640 left to budget in our Operating Expenses category for the quarter.

Now it’s up to us to decide how to allocate that remaining money.

If you’ve never budgeted before, you can look at your last one to three months of spending and see where your money goes, and enter the average amount into that sub-category under operating expenses.

Or, you can choose how much you want to spend from the different categories you create and then spend accordingly.

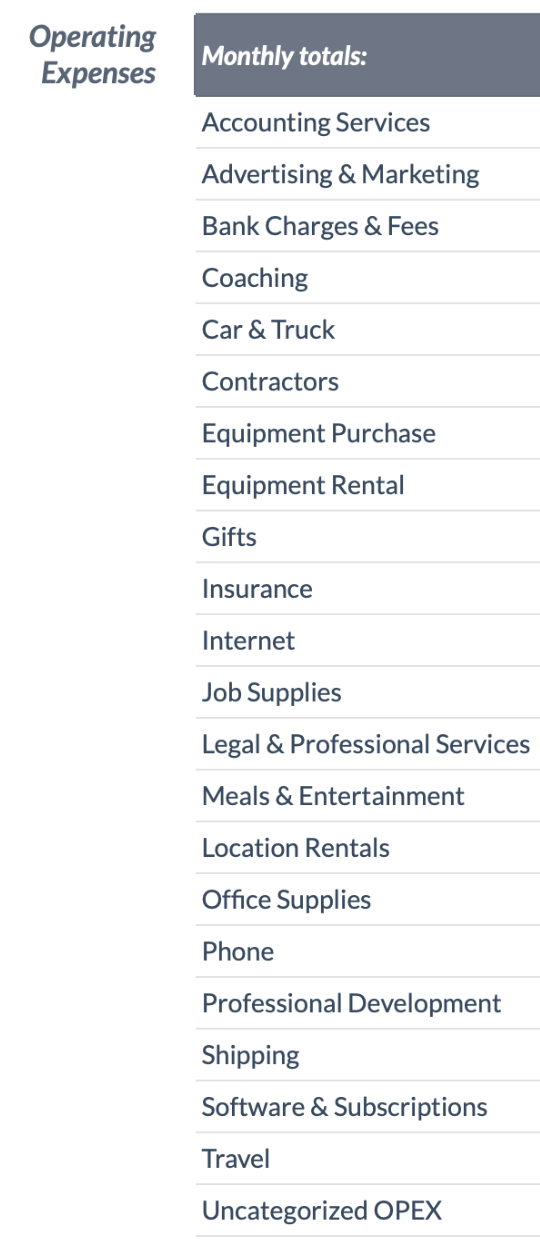

The next image shows some typical categories for creative businesses, but you can add or remove them to create a budget that makes sense for your business.

Now, we can divide the balance of $5,640 by three months to see that we have $1,880 to spend each month in the operating expenses category. You could end up with a budget that looks like this:

It’s always good to leave a little buffer in the “uncategorized” subcategory for the inevitable yet unexpected expenses that pop up each month.

Only Spend What You’ve Allocated

This is the part of budgeting many creatives and solo business owners could improve on, myself included.

Here’s an example of what we tend to do with our budgets.

An expense comes up like our hard drive is suddenly full and we have to go get a new one.

We check the bank account and see $2,874 in there, which is plenty to go and buy a new hard drive, so we head out to the computer store and get a nice big drive for $400.

Then, a few days later, an invoice for a contractor on our last project is due, for $2,500.

But we look at our account and realize there’s only $2,474 in there, so we can’t pay the invoice on time unless we move some money around.

We know that some money is coming in from a client in a few days, so we borrow some money from our personal account, or a credit card, pay the invoice, and are left with no money in our bank account for a few days.

When the client invoice comes in, expenses have been piling up so we rush to pay off the credit card, replenish our personal account, and then deal with the next bill in the stack.

It’s all very reactionary, hectic, and stressful.

Now, we need to stop operating this way as quickly as possible. With this new budget in place, we know how much we have to spend on different parts of our business.

While we may have $2,874 in our account, we need to look at our budget for the month to see how much money has been spent from the equipment purchases subcategory, and if there’s not enough for a $400 hard drive, we don’t buy the hard drive.

If that’s the case, then you can either buy a less expensive drive, or wait a month until you’ve saved enough in that category, or move money from another category to cover the larger expense.

But rather than looking at a single number—the available balance in your bank account—you need to consult your budget which gives more context to how much is available to spend in this specific category right now, how much money is already allocated for other expenses, and how much money is coming in.

Track Your Accounts Receivable

Speaking of money coming in, it’s important to stay on top of how much money is coming in over the next few months. This is known as your “accounts receivable”, which is the outstanding invoices that have been sent out to clients and customers but have not yet been paid.

As you’re projecting out over the next three months, it’s important to know if you’re potentially expecting a month where your income is lower than your planned expenses. If that happens, you have two options:

- Cut your expenses for the month

- Make more money

Yes, I know it sounds a little facetious, but I’m being serious. You are the owner of your business, and if you spend more than you make you’re destined for bankruptcy.

That’s why we want to be profitable from the start, but also profitable for as long as our business exists.

If you set up an accounts receivable tracking system, whether using Quickbooks or YouNeedABudget.com or your spreadsheet, you’ll have months to adapt and take action, rather than reacting to a situation that just happened.

If you know you have some big expenses coming up like travel or contractors or purchases, and your income isn’t sufficient to cover those increased amounts, then you need to make plans on how you’re going to deal with the situation.

If you plan to make more money, then come up with a list of ideas on how to get a few more projects, increase sales on the lower-rung projects on your sales ladder, or get paid sooner from a future client.

I highly suggest that you avoid things like debt, gap or bridge loans, invoice factoring, or anything else where you’re borrowing money to pay for something now, and then having to pay interest later.

Think of that debt interest as your profit, and wave goodbye to your profitable business.

While 5-10% interest may be small, if you’re only taking 2-5% profit in your business, you just spent your profit by paying back that interest.

Credit cards are even worse as they can run into the teens and twenties, interest rate wise, which can dramatically impact the profitability of your business.

In a movie, instead of “categories”, I have “departments” —an art department, camera department, production department, and more. (There can be dozens of departments on bigger films).

I give each of these departments a budget for the movie that they have to spend, and they don’t get to go over that budget. If they think they might, it’s my job to either prevent that overspending or move money from other areas of the budget to cover it.

In a film, you don’t want to have to go back to the financiers and ask for more money. It shows that you didn’t budget properly, or anticipate the spend in a timely enough manner, and if you have to get more money from them it often comes at a premium—15% or more.

That decision eats into the profitability of the film and makes it harder for the movie to make money through a sale or distribution deal.

The same is true for your business.

Budgeting is about planning and anticipation. You plan months ahead and allocate money to be spent so that you know you have enough for each category of spending. Then you focus some of your time on a few months ahead and adjust your budget each month, either putting more into profit, cutting expenses, or finding ways to increase your revenue.

I recommend that every quarter you adjust your numbers. See if you can cut your operating expenses a little. Increase how much money you put aside into profit, raising it by 1% every quarter until you feel like you have a comfortable amount sitting in that account. Then, you get to do something fun for yourself.

Your Business Should Pay You Dividends

Every quarter, your business is going to pay you a dividend. This is your business giving you a gift for being profitable.

Take 50 percent of the amount that you’ve set aside for profit and pay it to your personal account.

This is not income, this is a bonus.

You get to spend it on whatever you want—a nice meal with your partner or family, a new watch, a trip, an experience, it’s up to you! It’s a perk of owning your own business that most creators never afford because they never set aside any profit.

In the first year that I started setting aside money as profit, I bought myself an $80 smartwatch, some equipment for a backpacking trip, a new computer screen, and an iPad. Imagine what you would do with a nice $100, $1,000, or even a $10,000 quarterly dividend!

The other nice thing that will happen with you setting aside money for taxes is that you can pay quarterly taxes for both your business and your personal taxes! Your business can take care of you in more ways than one when you budget for it.

Plan out a budget for the next three months.

Allocate every dollar by giving it a “job”.

Track your spending weekly to see how much of each category you’ve spent, and make sure not to overspend in any category without being able to cover it from another part of your budget.

Anticipate 1-3 months out to see how much you plan to make and how much you plan to spend.

Adjust your budget every quarter to set more aside for profit and pay yourself a dividend.

Budget your business like a movie and you’ll always have enough to be profitable, and enjoy the benefits of having a business that you’re financially managing like a film producer.

Member discussion